Overview

The aim of this note is to explain some of the new VAT rules that overseas sellers will need to follow after Brexit. In this context an overseas seller is a business that is established outside of the UK and doesn’t have an establishment within the UK. The changes are reasonably complex because there are a number of changes that are happening simultaneously (Brexit, online market place rules, etc). Throughout this note OMP means overseas market place (ie Amazon).

A note of caution

I have spent quite a lot of time studying the guidance and I am not 100% sure that I have fully understood everything. I don’t think I am unique in this – I have consulted with a few experts, who seem as confused as I am. So please read what follows with some caution, and please let me know if you spot anything that seems not quite right. Hopefully things will clarify over time.

Index

This note is split into the following broad captions

- 1. Value of goods is less than or equal to £135

- 1.1. Summary of treatment – goods are located in the UK

- 1.2. Summary of treatment – goods not located in the UK

- 2. Value of goods is more than £135

- 2.1. Summary of treatment – Importer of record

- 2.2. Summary of treatment – not the importer of record

- 3. How to calculate the £135 threshold

- 4. References

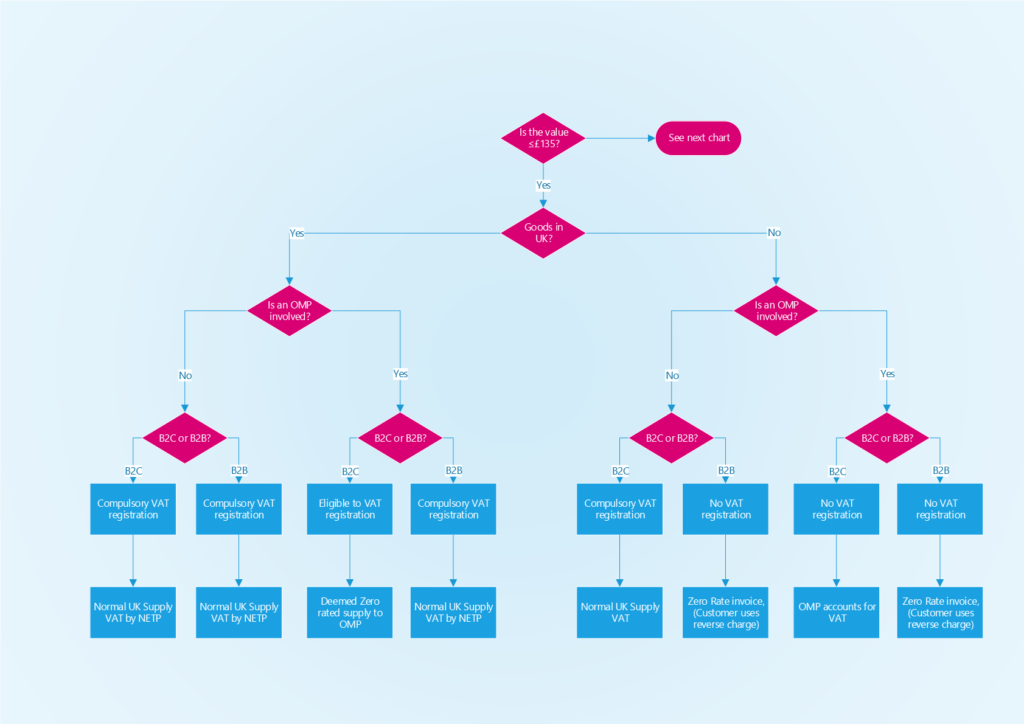

1. Value of goods is less than or equal to £135

The decision tree below shows the VAT requirements in the case that the value of goods is less than or equal to £135.

Decision tree – value of goods is less than or equal to £135

1.1. Summary of treatment – goods are located in the UK

First, lets look at the situation represented by the left hand side of the decision tree above – Where goods are held in the UK by the overseas seller.

a. Registration requirements

In all of the cases on the left hand side of the decision tree (where goods are held in the UK) the overseas seller will need to register for UK VAT. This is because of the general VAT rule – an overseas seller must register for UK VAT if it: 1) does not have a UK establishment; and 2) holds goods in the UK for sale. In this case there’s no VAT registration threshold and the overseas seller must register and account for UK VAT as soon as it holds stock for sale in the UK. Actually, there is an exception to this (the third case on the left). In this case (B2C sale facilitated by an OMP) UK VAT registration is optional (not mandatory). However, in most cases a business in this position will want to register for VAT so that it can reclaim the UK import VAT.

b. Consider as two movements

Remember, we are looking at the situation represented by the left hand side of the decision tree above – where goods are held in the UK by the overseas seller. In all four of these cases it’s useful to consider the sale as two movements of goods.

- The first movement – from abroad to the UK warehouse; and

- The second movement – from the UK warehouse to the UK customer.

c. The first movement – to the UK

Lets look at the first movement – from abroad to the UK UK warehouse. This is an import of goods and Import VAT is payable by the overseas seller. The Import VAT does not need to be paid when the goods cross the UK border (as used to be the case before Brexit). Instead, the VAT payment can be made through the UK VAT return. If we think about the invoice and the UK VAT return:

- Invoice: The overseas seller zero-rates the supply using its overseas VAT number

- UK VAT return: The overseas seller completes the boxes as follows:

- Box 1 – VAT due on imports accounted for through postponed VAT accounting

- Box 4 – VAT reclaimed on imports accounted for using postponed VAT accounting

- Box 7 – Total value of imports, not including VAT

d. The second movement – to the final customer

The treatment of the second movement – from the UK warehouse to the final customer – depends on the situation (see the decision tree above).

d.1. B2C and B2B supply of goods where there is no OMP

Let’s think about the invoice and the UK VAT return for B2C and B2B supplies of goods where there is no OMP:

- Invoice: The overseas business issues a normal UK VAT invoice (with its UK VAT number) to the final customer

- UK VAT return: The overseas seller completes the boxes as follows:

- Box 1 – The VAT due on the sale

- Box 6 – Total value of the sale, not including VAT

d.2. B2B supply of goods where there is an OMP

Now lets look at a B2B supply of goods where there is an OMP. In this case the overseas seller is responsible for accounting for VAT. The business customer should provide its UK VAT registration number to the OMP and the OMP should then give this to the overseas seller. The overseas seller then raises an invoice to the customer and records the VAT in the usual way, as follows:

- Invoice: The overseas business issues a normal UK VAT invoice (with its UK VAT number) to the final customer

- UK VAT return: The overseas seller completes the boxes as follows:

- Box 1 – The VAT due on the sale

- Box 6 – Total value of the sale, not including VAT

If the OMP doesn’t get the business customer’s VAT number then the OMP needs to treat the sale as a B2C sale (see d.3. below).

d.3. B2C supply of goods where there is an OMP (Deemed zero rated supply)

Let’s look at the case of a B2C supply of goods where there is an OMP. As I mentioned above, in this case the overseas seller is eligible (but doesn’t have to) register for UK VAT. However, it will normally register for VAT because this will allow it to recover its import VAT. The other difference in this case is that the OMP (not the overseas seller) is responsible for the UK VAT. The OMP is deemed to be the supplier and needs to pay the VAT. This means that for VAT purposes its not the overseas seller that is invoicing the final customer, its the OMP. Instead, the overseas seller is said to be making a ‘deemed zero-rated supply of goods to the OMP’. Assuming that the overseas seller is UK VAT registered it will account for the sale on its VAT return as follows:

- Invoice: The overseas business issues a zero rated invoice (with its overseas VAT number) to the OMP

- UK VAT return: The overseas seller completes the boxes as follows:

- Box 6 – Total value of the sale, not including VAT

Note that in this case Box 1 does not have to be completed by the overseas seller.

1.2. Summary of treatment – goods not located in the UK

Now lets consider the right hand side of the decision tree. These are the cases where goods are shipped directly from abroad to the UK.

a. B2C sales not facilitated by an OMP

Think about B2C sales not facilitated by an OMP. In this case UK VAT registration is compulsory. VAT is charged at the point of sale.

- Invoice: The overseas business issues a normal UK VAT invoice (with its UK VAT number) to the final customer

- UK VAT return: The overseas seller completes the boxes as follows:

- Box 1 – The VAT due on the sale

- Box 6 – Total value of the sale, not including VAT

b. B2C sales facilitated by an OMP

When a B2C sale of goods is facilitated by an OMP then it’s the OMP, not the overseas seller, that needs to register for UK VAT and pay UK VAT. The overseas seller just makes a zero rated supply to the OMP. UK VAT registration is not permitted. In this case:

- Invoice: The overseas business issues a zero rated invoice (with its overseas VAT number) to the OMP

- UK VAT return: There is no UK VAT return because the overseas seller is not UK VAT registered

c. B2B sales (direct and facilitated by an OMP)

For B2B sales (both direct sales and sales facilitated by an OMP) the system is the same as in the pre Brexit world. Namely the overseas seller zero rates the invoice and the UK business customer accounts for the VAT using the reverse charge procedure. Consequently, there is no requirement (or indeed option) to register for UK VAT. Where there is an OMP involved the OMP needs to get the business customers VAT number and pass it on to the overseas seller. If the business customer doesn’t give its UK VAT registration number, then the OMP will treat the sale as a B2C sale and follows the rules in 1.2.b. above. The invoice and VAT return entries for B2B sales are as follows:

- Invoice: The overseas business issues a zero rated invoice (with its overseas VAT number) to the final customer

- UK VAT return: There is no UK VAT return because the overseas seller is not UK VAT registered

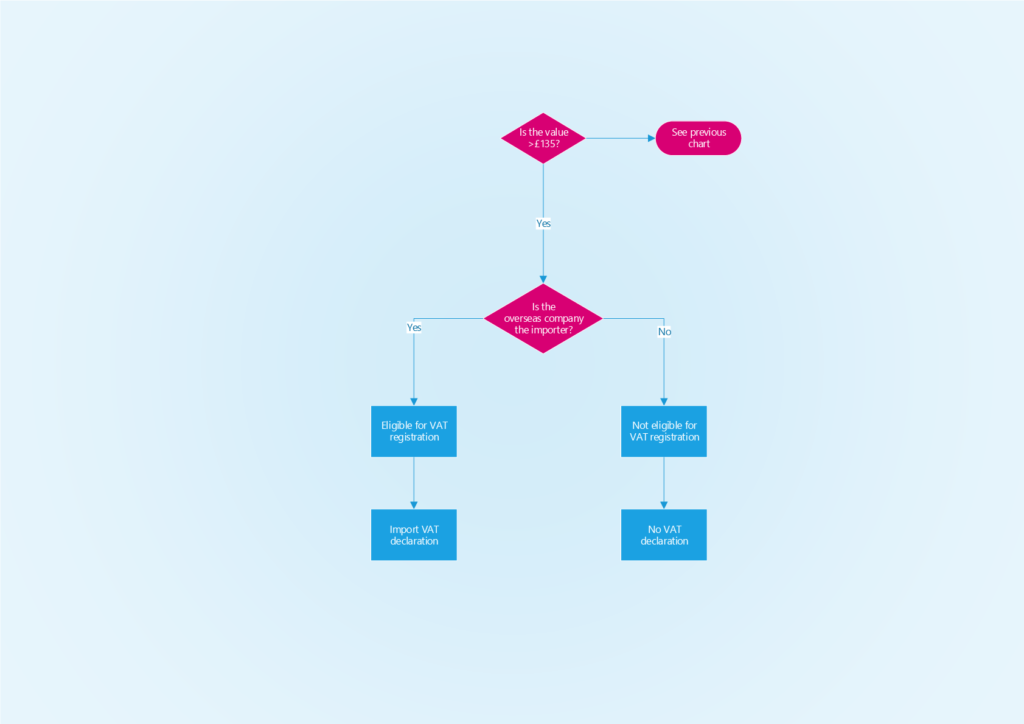

2. Value of goods is more than £135

The decision tree below shows the VAT requirements in the case that the value of goods is more than £135.

Decision tree

2.1. The rules pre-Brexit

Pre Brexit, goods imported into the UK from countries outside of Europe were held at the border, or at a postal collection office, until the VAT and duties was paid. Either the customer or the seller (if the goods were delivered duty paid) would pay this.

Importer of Record

The business (or person) responsible for paying import VAT and customs duties is called the ‘Importer of Record’. Lets imagine the situation where a US company imports goods into the UK. In this case the US company needs to make arrangements for the VAT and duties to be paid at the UK border. The business could either pay them, or ask his freight forwarder to pay them on his behalf. In either case he will have to pay the VAT (either to HMRC or to his freight forwarder). To evidence payment HMRC will send him a Certificate C79. If the US company is UK VAT registered, he would use form C79 as support to claim back the import VAT.

2.2. The rules post Brexit

Post Brexit, there are some major changes to the way import VAT works:

- EU countries need to pay Import VAT

- Import duties are only payable on consignments of more than £135

- For the period 1/1/21 to 30/6/21 UK VAT registered businesses don’t need to pay Import VAT at the border

The first two points above are fairly self explanatory. The third one needs some explaining.

2.3. Postponed VAT accounting

The first concept that one needs to understand is called ‘Postponed VAT Accounting’. Postponed VAT accounting means that the payment of VAT can be postponed – VAT doesn’t need to be paid when the goods enter the UK, instead it is paid when the VAT return is submitted. The intention is that Postponed VAT Accounting can be used up to 30/6/21. Businesses can use Postponed VAT Accounting and account for import VAT on their VAT returns if they are:

- the importer of record; and

- registered for UK VAT; and

- using the goods imported for their business use or for resale,

Sometimes postponed VAT accounting is optional and sometimes it is compulsory. As before, its convenient to consider the transaction as two movements of goods. The first movement – from abroad to the UK warehouse; and the second movement – from the UK warehouse to the UK customer.

2.4. For the first movement – from abroad to the UK warehouse

- Invoice: The overseas business issues a zero rated invoice (with its overseas VAT number)

- In its UK VAT return it completes the boxes as follows:

- Box 1 – VAT due on imports accounted for through postponed VAT accounting

- Box 4 – VAT reclaimed on imports accounted for using postponed VAT accounting

- Box 7 – Total value of imports, not including VAT

2.5. For the second movement – from the UK warehouse to the UK customer

- Invoice: The overseas business issues a normal UK VAT invoice (with its UK VAT number) to the final customer

- UK VAT return: The overseas seller completes the boxes as follows:

- Box 1 – The VAT due on the sale

- Box 6 – Total value of the sale, not including VAT

2.6. Compulsory postponed VAT accounting

If you import ‘non controlled goods’ goods into the UK from the EU between 1 January and 30 June 2021, you must account for import VAT on your VAT Return if you either:

- delay your customs declaration; or

- use a simplified customs declaration to make a declaration in your own records.

If you complete a supplementary customs declaration you need to select that you’ll be accounting for import VAT on your VAT Return.

Optional postponed VAT accounting

You can opt for postponed accounting if :

- the goods you import are for use in your business

- you include your VAT registration number on your customs declaration

In this case you need to tell your customs agent that you want to account for import VAT on your UK VAT Return. Your agent will need to select this on your customs declaration and enter your details and your VAT details as the consignee.

3. How to calculate the £135 threshold

We’ve spoken about the £135 threshold quite a lot. The threshold comes from EU legislation €150 and is based on the price at which the goods are sold, excluding:

- transport and insurance costs, unless they are included in the price and not separately indicated on the invoice;

- any other taxes and charges identifiable by the customs authorities from any relevant documents.

Note that the £135 applies to the value of the consignment, not to each individual item within the consignment.

4. References

- VAT and overseas goods sold to customers in Great Britain using online marketplaces from 1 January 2021

- Check when you can account for import VAT on your VAT Return from 1 January 2021

- Complete your VAT Return to account for import VAT from 1 January 2021

- How to fill in and submit your VAT Return (VAT Notice 700/12)

- Changes to VAT treatment of overseas goods sold to customers from 1 January 2021

- UK VAT on eCommerce legislation

Overview The aim of this note is to explain some of the new VAT rules that overseas sellers will need to follow after Brexit. In this context an overseas seller is a business that is established outside of the UK and doesn’t have an establishment within the UK. The changes are reasonably complex because there are […]